A corporation offers both opportunities and challenges as a mode for running a business.

Low tax rates apply to its active business income, allowing more earnings to be reinvested in the growing enterprise. Its continued success may then lead to surplus cash beyond business needs, but our tax policies are not so friendly when it comes to corporate investment income.

What if there’s an alternative way to manage this money that circumvents these punitive tax rules?

While small business tax rates for corporations are in the 10-15% range, investment income may be subject to rates closer to 50%.

The excess tax levy is essentially a zero-return deposit with the Canada Revenue Agency, known as refundable dividend tax on hand (RDTOH).

A corporation can recover this RDTOH, but only

as taxable dividends are paid to shareholders.

And to get the investment principal out, again taxable dividends are usually required.

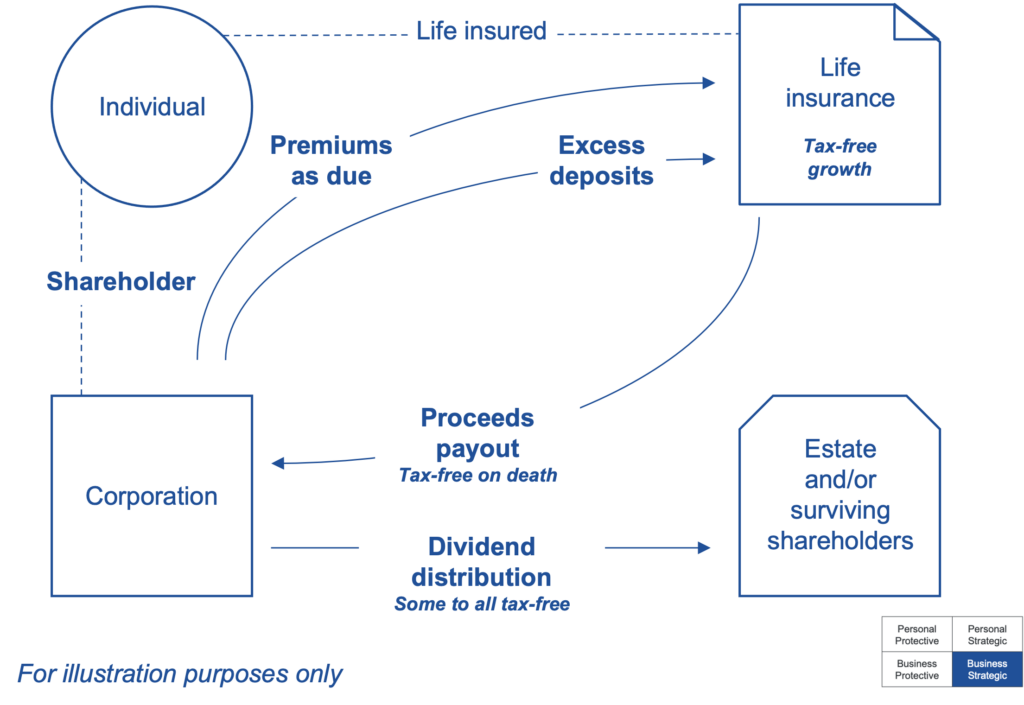

In contrast to traditional investments, certain life insurance policies can grow tax-sheltered. This applies to deposits in excess of the premiums required to keep the policy in-force.

At death, the policy – including the tax-sheltered growth – pays out tax-free to the corporation.

A mechanism called the capital dividend account (CDA) tracks such tax-free corporate receipts. This CDA credit allows for tax-free dividends to pass most to all of the insurance to estate beneficiaries.

Based on an established insurance need, the corporation is owner, payor and beneficiary.

Surplus corporate cash is annually re-directed from taxable investments into the tax-exempt policy. An executed shareholders’ agreement will bind the corporation to distribute the tax-free insurance proceeds to the estate beneficiaries.

The insurance company’s software can illustrate the increased internal rate of return (IRR) offered by the insurance over taxable investments.