Tag: Corporation

When does corporate cash become investible?

Operational efficiency to investible surplus

Apart from pursing a passion, the purpose of running a business is to generate income. To the point, eventually you intend on spending what your hard work produces, and using the excess to invest in yourself and your future.

Sometimes the route from contributed capital to surplus cash is quick, direct and transparent. More often though, invested cash takes on a variety of forms as it travels through the enterprise before emerging as profit. How complex that route is and how long it takes depends on the scope and scale of the business.

That being the case, it can be difficult to determine when, where and how to use portfolio investments in a corporation.

That being the case, it can be difficult to determine when, where and how to use portfolio investments in a corporation.

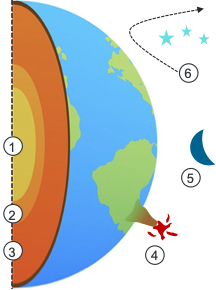

It may help to use the analogy of the earth and its gravitational pull to follow the movement of cash through a corporation.

Operational efficiency – Running the business

1. Inner core

Cash cycles through current assets such as prepaid expenses, inventory, and accounts receivable, and is applied to current liabilities as they come due. Some may be held in physical currency, but its use is more practically facilitated through deposits and short-term credit tools.

2. Outer core

Working capital is the continuous float – the ebb and flow between current assets and liabilities – that keeps a business running. Usually it is supported by a revolving line of credit so that the owner can focus on the business, and not accounting balances.

Working capital is not itself investible, but to the extent that efficiencies are applied (eg., timely use of payment terms, prompt account collections, optimal inventory levels, smart foreign exchange practices, etc.), more cash may be freed up to move up and out of a corporation.

3. Mantle & crust

Long-term assets are the structure within which the business produces its wares. They last for many years, but eventually have to be replaced in order to sustain productive capacity.

The cost of replacement is commonly managed through a combination of asset-backed loans and capital reserves. To assure that reserves are available when needed, safety and liquidity are the top priorities.

Investible surplus – Breaking the business’ gravitational pull

4. Surface

Retained earnings is the after-tax money of the corporation. The portion of it that is not needed for business operations or capital reserves may be appropriate for passive portfolio investment.

5. Orbiting

A holding company may receive tax-free inter-corporate dividends on shares it holds in an operating company. This puts the extracted funds beyond the reach of operating company creditors, so may be a preferred place for portfolio investments. Where there is more than one business owner, each might establish a holding company so that respective funds and investment portfolios may be isolated.

6. Beyond gravity

Dividends to a shareholder may be placed in a personal non-registered investment account. Such dividends are taxable, meaning the personal investible amount is less than if it remained in a corporation. On the other hand, investment returns are taxed less favourably in a corporation, and sooner or later will have to cross that threshold for shareholder personal use. Tax advice is a must.

Corporate investment portfolios – Opportunities and obstacles

Informing your returns by understanding passive tax rules

The taxation of passive income in corporations is a very complex topic. The intention here is to provide a general overview to help you discuss with your accountant and your investment advisor how this may apply in your circumstances.

As the owner of a corporation, you know your active business income is taxed at a rate that is usually well below your personal rate. Presumably, that’s part of the reason you are using a corporation in the first place.

Top personal tax rates are near or beyond the 50% mark, but general corporate rates are in the area of 26% to 31%, and small business corporate rates (on active business income up to $500,000 in most provinces) range from 9% to 15%. The variance depends on the provincial rates where a corporation is resident, with federal rates being consistent across the country.

Is passive income tax-preferred in a corporation?

In a single word, the answer is “no”, but it’s much more complicated than that.

For active business income, those lower corporate rates allow more after-tax cash to be reinvested in a business that is run through a corporation. The public policy purpose is to help businesses grow.

However, those low rates do not extend to non-business income earned in a portfolio – known as passive income – such as interest, dividends (Canadian or foreign) and capital gains. So, if passive income isn’t entitled to reduced tax rates, why invest in a portfolio within a corporation?

There’s more investible money if it stays in the corporation

When you use a corporation, income tax is charged first at the corporate level, with the net-of-tax amount added to the corporation’s retained earnings. Those retained earnings are eventually distributed as taxable dividends to shareholders. To protect taxpayers from double-taxation, the arithmetic is designed so that a shareholder’s personal tax on a dividend is reduced by the amount that the corporation has already paid.

Note though that a corporation is not required to immediately distribute its retained earnings. Apart from reinvesting in the business as noted above, those funds could go into a passive investment portfolio. As compared to paying a dividend (reduced by the associated tax) and investing in a personal portfolio, there will be more dollars to invest if the portfolio is at the corporate level.

But … the public policy response

As more can be invested at the corporate level, proportionately more passive income could be earned there. While this is understandably appealing to a shareholder and corporation, from the policymaker’s perspective it is an unintended consequence of this two-stage system: The use of the corporation as a more efficient form for business growth has arguably led to an extra benefit for earning passive income.

Emulating top personal tax rates

In response, additional corporate tax is imposed, making it less appealing to invest corporately. The additional tax takes the corporation approximately to the top personal tax bracket rate. Much of that extra tax is refunded to the corporation (see RDTOH following) when later dividends are paid – but not necessarily all of it. Again, it varies by province, and also by the type of income earned. For example, the combined corporate and personal tax can be 4% to 8% higher on interest earned through a corporation, as compared to earning interest in a personal portfolio.

The (intended) equalizer: Refundable-dividend-tax-on-hand

Historically, that extra tax has been tracked in the corporation’s refundable dividend tax on hand (RDTOH) account. In truth there are two RDTOH accounts, depending on whether the original income was charged the general corporate rate or the small business rate, but for simplicity in this article we’ll refer to it in the singular. Either way, RDTOH is effectively a deposit with the Canada Revenue Agency (CRA) that earns no income. Most taxpayers aren’t so generous to make such interest-free loans to the CRA, and that’s why it’s usually a priority to get that money back – refunded – so that it can be put back to work in the corporation, whether that’s as a business reinvestment or an addition to a passive portfolio.

When a taxable dividend is paid to a shareholder, a portion of the RDTOH balance is refunded to the corporation. The current refundable rate for present purposes is 38 1/3%, but a simpler way to express it (as a rough estimate) is that for every $5 dividend paid from the corporation to a shareholder, about $2 comes back to the corporation from its RDTOH.

Previously, any taxable dividend could recover refundable tax. As of 2019, refunds are generally only paid on dividends where the original corporate income was charged the small business rate (non-eligible dividends) or where it arises out of the corporation’s passive investment income.

Reduction in small business deduction threshold

A further implication of earning passive corporate income is the potential reduction in how much active business income (ABI) is entitled to the small business deduction (SBD) or rate. The SBD is available on income up to $500,000, but for every $1 of annual passive income, that threshold is reduced by $5. That means that if passive income exceeds $150,000 in a year, all active business income will be charged the general corporate rate.

What’s a shareholder to do?

As much of a challenge as all this presents, all is not lost for corporations and their shareholders.

First, your corporation pays no tax on Canadian dividends that are passed through to you as shareholder. Those dividends maintain their preferred tax treatment, the same as if the security had been in a personal portfolio. And as more dollars are available to be invested at the corporate portfolio level, as discussed above, more of those Canadian dividends can be generated.

Second, a corporate portfolio that grows through unrealized capital gains defers income realization. This in turn delays application of the passive rules. Ideally the portfolio would remain intact until there is a personal need for the funds. By cashing out the investment at the same time as an intended dividend, there will be minimal, if any, inefficient refundable tax balance.

Third, only a portion of capital gains are taxable, with the non-taxed portion able to be paid as a tax-free dividend. The current income inclusion rate is 1/2, with the corollary that the non-taxed portion is also 1/2.

And finally, a shareholder is likely to be at a lower tax bracket in later years. By consciously leaving an appropriate amount in a corporate portfolio, tax can be both deferred and reduced.

As always, tax should not be the primary consideration when investing. It can however have an especially large impact when income is originally earned in a corporation. With awareness of the passive tax rules, you can have a more informed conversation with your accountant and your investment advisor about how to manage your corporate portfolio.