A tax tool for comparing interest to other investment returns

Rate of return on a portfolio is often front and centre in an investor’s mind. Understandable as this is, ultimately it’s about how much of those returns the investor will keep. The difference between the two is tax, which in turn depends on the type of income earned and the investor’s tax bracket.

This article deals with an individual earning income in a non-registered account, also known as an open account or cash account. With a range of variables in play, it can be difficult to follow the steps from initial return through tax calculation to spendable after-tax cash. A useful tool to help connect the arithmetic is interest equivalency.

Interest – Taking into consideration the tax trade-off

Interest is appealing for the part of a portfolio where certainty is the prime concern. For example, the issuer of a guaranteed investment certificate (GIC), agrees to pay a set amount of interest for the period of the contract.

This certainly provides valuable comfort to the investor, but an important trade-off from a tax perspective is that interest faces the full tax rate at any given income bracket.

Preferred taxation – Capital gains & Canadian dividends

Compared to interest, Canadian dividends and capital gains receive favourable tax treatment. They come at it from different routes, with the benefits emphasized at different income levels. Canadian dividends provide the best after-tax yield at low to mid brackets, giving way to capital gains at higher and top brackets.

Capital gains

There are two features that lead to the favourable tax experience from capital gains:

-

- Deferral – While a security is held, no tax arises on changes in its price. This is also true if the investor holds a mutual fund that fluctuates according to price movement of its underlying securities. But a redemption/sale is a taxable event, and if the value has increased then the investor will realize a capital gain at that time.

- Reduced inclusion rate – When there is a disposition, capital gains are said to be realized in that year, but only a portion of the capital gain is taxable. The “taxable capital gain” is derived by applying the income inclusion rate, which has ranged between 1/2 and 3/4 since 1971, but has been stable at 1/2 since 2000. The 2024 Federal Budget increased it to 2/3, while still allowing the 1/2 rate on the first $250,000 of an individual’s annual capital gains. (For trusts and corporations, the 2/3 rate applies to all capital gains.) The 1/2 rate is used in the examples to follow, on the assumption that the investor is an individual with less than $250,000 of annual capital gains.

The first feature allows tax-deferred growth. It is the second that is used in the interest equivalency calculation.

Canadian dividends

Like interest, Canadian dividends are taxed in the year earned, but the tax is calculated in two steps:

-

- Gross-up – The ‘gross-up’ factor adds back the corporate tax, so the investor’s bracket can be used to calculate the tax as if the investor had earned the income that was really earned by the corporation.

- Tax credit – The investor then gets a tax credit for the tax that the corporation has already paid.

This two-step process protects against double-taxation. The government’s revenue is split between the corporate tax and the personal tax, which is why an investor pays less on a dividend compared to the full rate for interest.

How interest equivalency works

Interest equivalency shows what amount of preferred income will give an investor the same after-tax spendable cash as a dollar of interest. Alternatively, it can be expressed as the higher amount of interest that equates to a dollar of preferred income. Either way, the result is expressed in dollars and cents.

Formula

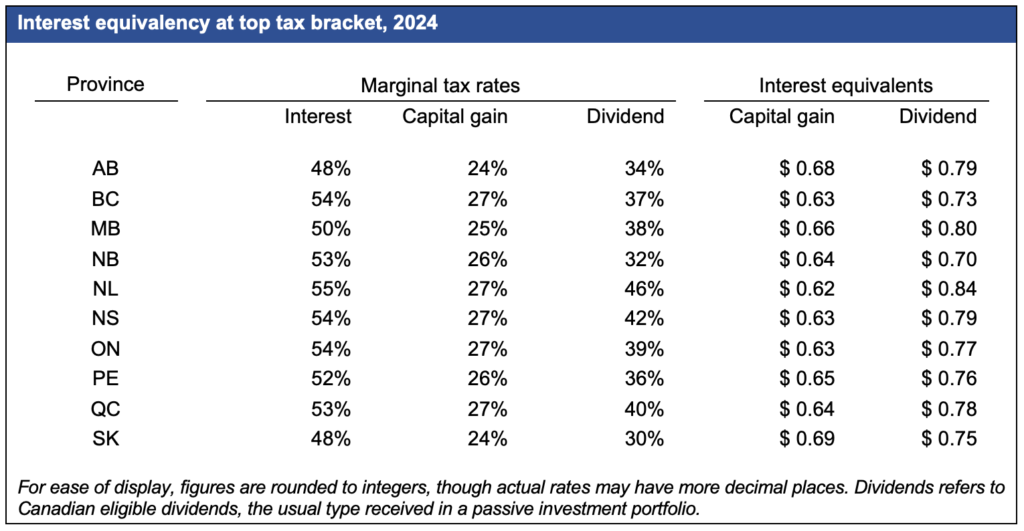

Interest equivalency is shown in the following table at top tax bracket for each province, but it can be calculated at any income level by applying the following formula that uses marginal tax rates (MTR):

Interest equivalency = ( 1 – MTRinterest ) ÷ ( 1 – MTRpreferred )

Proof

It may be easier to see how this works by looking at an example, here using Alberta in the first row of the table:

Informing yourself with this tool

To be clear, interest equivalency is a tool used to compare investment returns; it is not a suggestion against interest returns in a portfolio. All income types have their respective features, benefits and risks. The tool can help advisors and investors understand, compare and discuss investment options and recommendations in a portfolio.