Re-directing final tax dollars to your chosen causes

As a regular supporter of your favourite charity, you’re pleased that your annual donations help keep the lights on. Ideally though, you’d also like to contribute in a way that sustains the organization over the longer-term.

One way to do this – without reducing what you need to live on – is to direct some or all of the remaining value of your RRSP or RRIF on death to your chosen charity. Not only will that make for a substantial gift in and of itself, but you’ll also be pleased to know that it comes

‘at the expense’ of some of the tax that would otherwise have been paid at your death.

Indeed, after the tax break, the donation may only cost you half of what the charity receives.

Tax imposed on registered plans at death

For many Canadians, registered retirement savings plans (RRSPs) are the primary tool used to accumulate retirement savings. Contributions are tax-deductible, with income and growth tax-sheltered while in the plan.

Commonly on retirement, an RRSP is converted into a registered retirement income fund (RRIF), which continues to enjoy tax-sheltered income and growth. Withdrawals from the plan are taxable income, but usually spread over multiple years at graduated tax bracket rates.

Still, the entire value of a RRSP/RRIF is eventually taxable.

On death, the remaining balance is treated as income that year, though that can be deferred by rolling over to a registered plan of a spouse or financially dependent child or grandchild. Otherwise, the full amount is taxed in a single year, pushing up through those graduated brackets toward the top bracket, which is within a couple percentage points of 50% or more, varying by province.

Tax relief on charitable donations

When someone donates to charity, the person may claim a credit to reduce annual taxes. The tax credit is at the lowest bracket rate on the first $200 of donations claimed in a year, being 15% federally, and ranging by province from about 5% to 20% depending on where the donor resides.

Above $200 of annual donations claimed, the tax credit jumps to a higher rate. The high rate applied against federal tax is the 4th bracket 29% rate, or the top/5th bracket rate of 33% if income is over that level. Those brackets are $181,440 and $258,482 in 2026. For provincial tax, Quebec and BC use the federal approach, with the other provinces applying a single high credit rate that is near or equal to their top bracket rate. This puts the combined federal-provincial credit rate near or above 50%, varying by province.

The maximum annual donation that can be claimed is equal to 75% of a taxpayer’s net income. That limit is increased to 100% in the year of death, and if the donation is larger than that final year’s net income, the excess can be used to recover tax from the preceding year’s tax bill, also based on up to 100% of net income

Donating registered plans to charity at death

The owner of a RRSP/RRIF may designate one or more beneficiaries to receive the proceeds of a plan upon the person’s death. The plan administrator will provide a form to make that direct designation, or alternatively most provinces allow for a person’s Will to direct the proceeds of such a plan. (Note that direct designations are not available to Quebec residents, whether on the plan directly or by Will.)

A named beneficiary may be another person, or it may be an organization, such as a charity. When a charity is named, by either method, the donation is deemed to have been made immediately before the person’s death. This then qualifies the donation for that 100% threshold for both the year of death, and excess carryback to the preceding year.

Spousal flexibility

A spouse could be designated as primary beneficiary, with the charity named as contingent beneficiary. This assures that a living survivor would continue to have full use of the couple’s savings on a first death through the usual tax-deferred rollover. Meanwhile that contingent designation serves as a backup plan if the survivor forgets to name the charity as beneficiary after the first spouse’s death, or if there is an unfortunate common disaster.

Note that once a RRSP/RRIF has rolled to a spouse, the original owner’s instructions will have no further control over the proceeds. When carried out by beneficiary designation, the past plan ceases to exist, as does any contingent designation. When the transfer to the spouse is as successor annuitant on a RRIF, the plan and contingent designation may remain intact, but the surviving spouse has full legal control over the plan, including the right to change any designation.

Providing a legacy through the Will

Sometimes a person may be uncertain whether their estate will have enough liquidity to fund desired legacies, or even to commence administration of the estate. For example, some provinces require that the probate fee/tax is paid before the executor is granted legal authority to deal with estate property. Potentially a RRSP/RRIF could be made available for this purpose, either by foregoing the naming of a beneficiary for the plan, or by making a direct designation to the estate (on the plan or by Will).

Once the estate liquidity need has been satisfied, the net remaining funds could then be paid as a legacy to the charity. So long as the donation occurs within 36 months of the date of death, it may be claimed in the estate year when it is made or in an earlier estate year (in either case up to 75% of net income), or in the year of death or preceding year (once again, up to the 100% threshold).

Probate and estate creditors

The trade-off in allowing the RRSP/RRIF to come into the estate is that it will be subject to probate fee/tax in provinces where such applies, and estate creditor/claimants may latch onto those plan proceeds.

Comparatively, a direct beneficiary designation (other than to the estate) bypasses probate and creditors. This bypass generally applies even when the Will is the instrument used to make the designation, though this should be verified with the drafting lawyer, as probate has been levied in some provinces based on the facts in a few court cases.

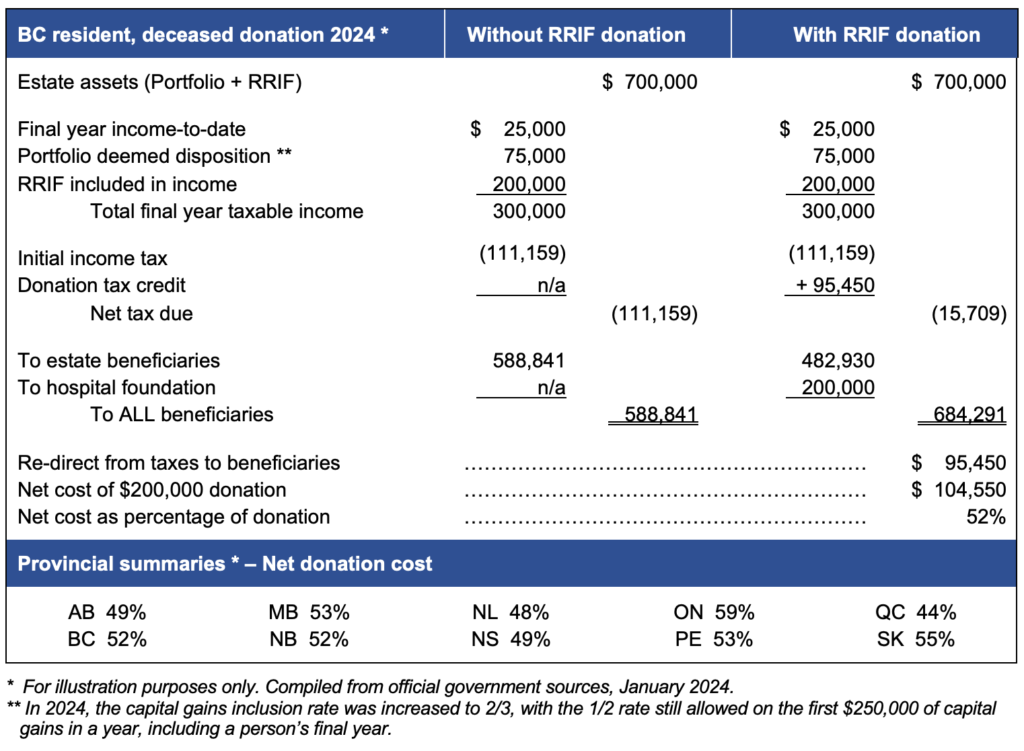

Illustrating donation of RRSP/RRIF on death

To illustrate how this can work, meet Greg who lives in British Columbia. He wants to give back to the local hospital that provided such compassionate support when his spouse Jean went through palliative care. He confirms the legal name of the hospital foundation, and names it as beneficiary on his RRIF administrator’s form.

Greg understands this will reduce how much will go to their children – all financially secure adults – but expects it will also reduce the estate tax bill, making it an efficient way to donate. On his death, Greg was living in long-term care, which consumed his $25,000 income to-date that year. On death, there was a $500,000 non-registered portfolio with a $150,000 capital gain (resulting in a taxable capital gain of $75,000, based on the 1/2 inclusion rate), and a $200,000 RRIF.