As a business’s founder ages, focus often shifts from building aggressively, to exiting safely.

Particularly for those slowing down as they move into their 70’s, this change may feel like being caught between a rock and a hard place. Is it possible to provide yourself with a tax-efficient lifelong cash flow, but still leave an estate that cushions the tax impact on spouse and family?

The Corporate Insured Annuity may be just the ticket to help achieve both goals.

Shareholders pay no tax on increasing value of corporate assets until shares are disposed, and even then only part of the capital gain is taxable.

Eventually though, without actually selling, the shareholder’s own death deems the shares to be disposed. A rollover to a spouse can delay that terminal tax bite, but otherwise it’s inevitable.

What if you could reposition assets for a guaranteed continuous cash flow, while taking their value out of that terminal tax calculation?

When a corporation receives proceeds from life insurance it owns on a shareholder, that does not add to the deemed disposition value of shares in the terminal year (except for any cash surrender value). This would normally be true for term-to-100 and minimum funded universal life policies.

Similarly, a corporate-held life annuity with no guarantee would add little to share value on death, with no payments coming thereafter. And the value will steadily decline as an annuitant-shareholder ages, especially in advanced years.

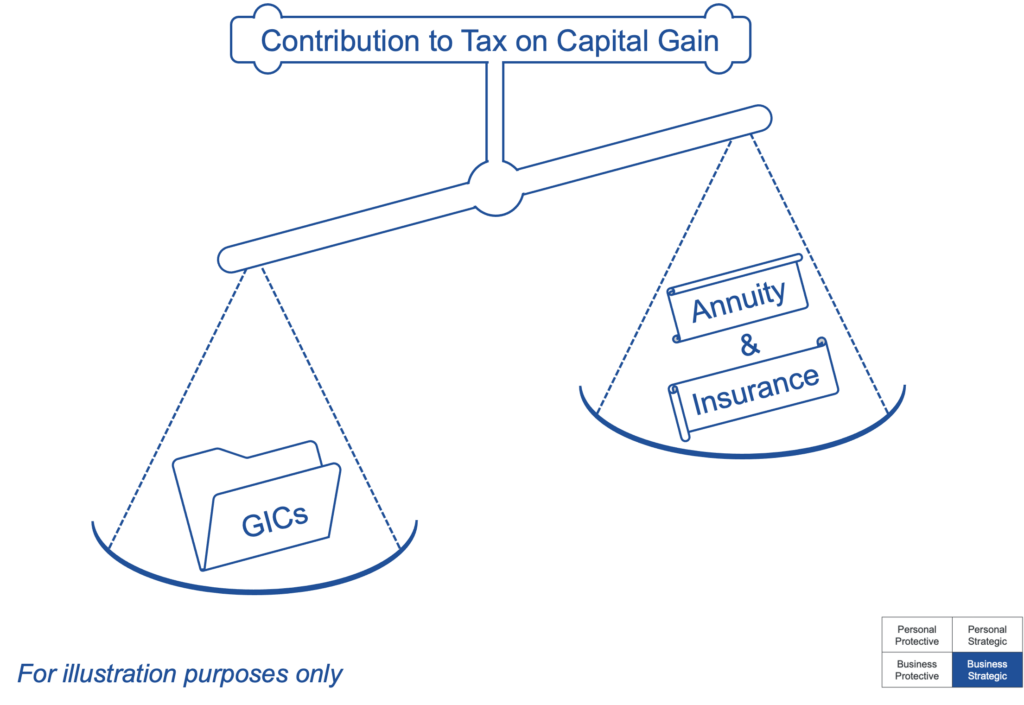

Like its counterpart on the personal side, a Corporate Insured Annuity can improve annual investment cash flow – for lifelong dividends to the shareholder personally – while guaranteeing the return of the invested capital on death.

Beyond that, the annuity and life insurance will contribute little more than a fraction toward the deemed disposition value of shares at death, compared to fully-counted holdings like chequing accounts, deposits and GICs. A lower capital gain means less terminal tax, and more estate.