Tax-sheltering disability savings, with a government boost

The Registered Disability Savings Plan (RDSP) is a long-term savings tool for a person who is eligible for the disability tax credit (DTC). It has three main financial benefits:

-

- Government money added to personal contributions

- Tax-sheltered growth of personal and government money in the plan

- Tax eventually borne by the plan beneficiary, not the contributors

Who qualifies to use a RDSP?

A RDSP may be opened by a person up to age 59 who qualifies for the disability tax credit, and is a Canadian resident with a valid Social Insurance Number (SIN). If the application is made (on the beneficiary’s behalf) by someone other than the DTC-qualified person, that applicant must also have a valid SIN. If at a later time the beneficiary no longer qualifies for the DTC, the plan may remain open but no further contributions are allowed.

There can only be one RDSP for a given beneficiary, and only one beneficiary for each RDSP.

How do you set one up?

Application is made to a RDSP issuer, which is a financial institution registered with the government to open plans, receive government bonds and grants, and invest funds as directed by the plan holder.

The plan holder will generally be a parent or guardian if the beneficiary is a minor. An adult beneficiary must be his/her own holder, unless he/she is not contractually competent, in which case it may be a parent, spouse or common law partner, qualifying family member or designated legal representative.

Allowable contributions and their tax treatment

The lifetime contribution limit is $200,000, but there is no annual limit. However, there are annual limits to the amount of government assistance (see CDSB and CDSG below), which could influence contribution timing.

Contributions are after-tax, meaning there is no tax deduction when contributing. Government assistance is not taxable when credited to a plan. While in the plan, there is no tax on income earned on either personal or government contributions.

RRSP rollovers

RDSP contributions may also be by a tax-deferred rollover from a deceased’s registered retirement savings plan (RRSP) or registered retirement income fund (RRIF). The beneficiary must be a child or grandchild who was, at the time of the deceased’s death, financially dependent on the deceased for support by reason of an impairment in physical or mental functions. These contributions are included in the $200,000 lifetime contribution limit but do not attract any matching grants, and will be included in the taxable portion of future RDSP withdrawals.

RESP rollovers

Funds in a registered education savings plan (RESP) may also be rolled over to a RDSP on a tax-deferred basis. The same person must be the beneficiary of the RESP and RDSP. This is an option under RESP rules, where an accumulated income payment (AIP) would otherwise be taxed currently. As with RRSP/RRIFs, such contributions are included in the $200,000 lifetime contribution limit but do not attract any matching grants, and will be included in the taxable portion of future RDSP withdrawals.

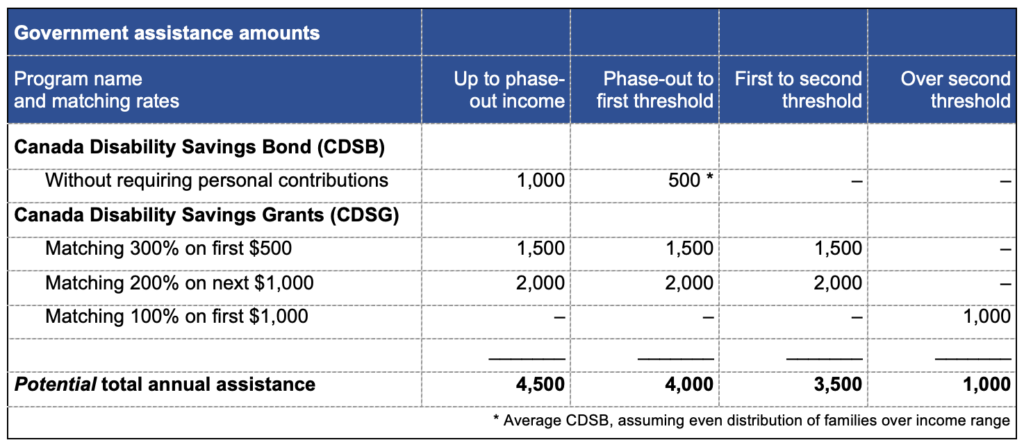

Government assistance: CDSB and CDSG

Though a RDSP may receive personal contributions up to age 59, government assistance through the Canada Disability Savings Bond (CDSB/bonds) and Canada Disability Savings Grants (CDSG/grants) are only available up to the beneficiary’s age 49.

The CDSB makes an annual payment to a RDSP, regardless of personal contributions. It can be up to $1,000 annually, with a lifetime limit of $20,000. If the beneficiary qualified for a RDSP in years before the plan was opened, a one-time catch-up up to $10,000 is allowed for unclaimed bond money over the preceding 10 years.

The CDSG matches personal contributions. It can be as much as a 300% match, to a maximum of $3,500 annually, with a lifetime limit of $70,000. Like bonds, up to 10 years of catch-up is allowed, but the maximum that can be received in any one year is $10,500 (or 3X maximum), so it may take a few years to collect all the matching grants.

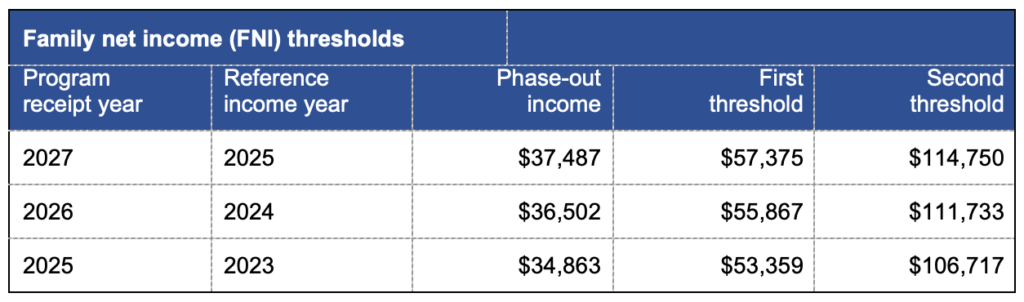

The amount available under these programs is determined according to family net income (FNI) thresholds two years preceding the program year, as shown in the table below. When a beneficiary is under 19, FNI is the combined net income of the beneficiary’s parents. Thereafter, it is the beneficiary’s own net income (even if continuing to live with parents), or if the beneficiary is cohabiting with a spouse or common-law partner then that couple’s combined net income.

There are three FNI thresholds used to determine the annual assistance amount:

- Phase-out income – The income level above which the annual amount of CDSB payable begins to decrease.

- First threshold – The income level that, when reached or exceeded, the annual amount of CDSB payable is nil.

- Second threshold – The income level that, when below or equal to, the matching grant will be 300% of the first $500 in contributions and 200% of the next $1,000 in contributions. When income is above this level, the matching grant will be 100% of the first $1,000 in contributions.

Effect on other public support

Having a RDSP will not affect eligibility for federal programs such as the Canada Child Benefit, GST/HST credit, Old Age Security or Employment Insurance, nor limit access to provincial disability support programs.

Withdrawing funds from the plan

Withdrawals are formally called disability assistance payments (DAPs), and may be taken periodically, or as annual recurring payments. Recurring payments are called lifetime disability assistance payments (LDAPs). LDAP payments must begin by the end of the calendar year that the beneficiary turns 60.

When a withdrawal is taken and CDSB and CDSG have been received in the preceding 10 years, a portion of those bonds and grants may be repayable. Repayment may also apply if the beneficiary is no longer qualified for the DTC and takes a withdrawal while under age 60.

There is no repayment of grant or bond money if the beneficiary has turned 60, if the last bond and grant money was received more than 10 years ago, or if reduced life expectancy is five years or less.

When assistance is paid to the beneficiary – who does not have to be a Canadian resident at the time – each payment is a proportion of personal contributions, investment earnings, CDSB and CDSG. The beneficiary is taxed on the payment except for the portion that represents the return of personal contributions.