As a business founder, you chose to be your own boss, devoting your skills into an enterprise designed to provide you with an independent income, and a home for your reinvested wealth.

As business progressed and assets grew, your thoughts will have gone from reaching breakeven, through sustaining profitability, and now on to (eventually) transferring to your successors.

Yes, blue skies are ahead, both for you and the business, but there are also clouds forming: taxes.

Like an iceberg, that appreciated value may be unseen or below the surface, until there is a sale or gifted transfer that triggers tax on the capital gain.

Fortunately, there is relief on share transactions and with farms or fisheries, where up to $1.275M of capital gains (2026 indexed) may be shielded under the lifetime capital gains exemption (LCGE).

But if your growth is beyond the LCGE, tax could still hamper your plans. It’s like your own success is getting in the way of extending and sharing your good fortune.

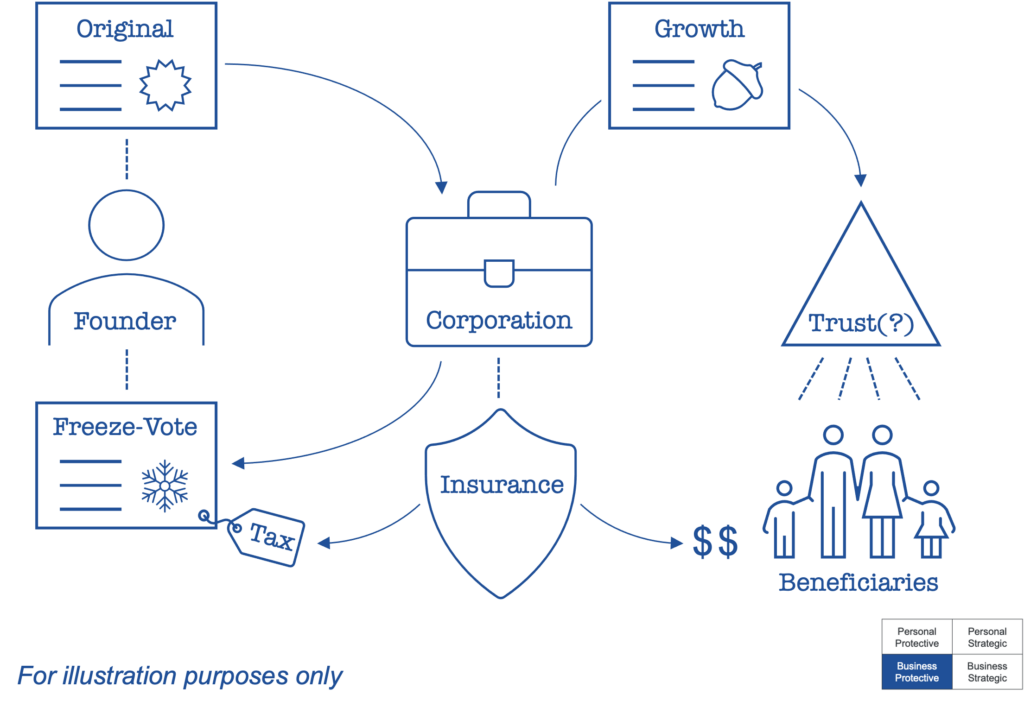

Wouldn’t it be nice to tell tax collectors, “Hold on!”? That’s an estate freeze: A tax-deferred business reorganization for the founder, with assurance that the next generation can take over … but not just yet.

The amount of tax on the transfer is frozen, with its payment delayed as far out as the founder’s death. Meanwhile, future growth accrues to successors, also pushing that tax bill years or decades ahead.

What makes it work is life insurance on the founder that exactly aligns with that postponed tax payment.

Freezes range from simple to complex, according to

the nature of the business, and the current needs and future intentions of the parties. Familiar elements are:

- Founder exchanges original shares for tax-deferred ‘freeze’ voting shares with same cost base & value

- Nominal value ‘growth’ shares are issued to successors, often via a trust with founder as trustee

- Corporation obtains life insurance on founder for an amount equal to the expected tax on the capital gain

- Alternatively, insurance may be joint-last-to-die with founder’s spouse, and/or may be personally-owned

- If some freeze shares are retired during founder’s life, excess insurance not needed for tax can go to heirs