Successful business owners don’t just sit idly by, pondering possibilities – they monetize their imagination. They identify opportunities, assess risk and commit their capital to realize their vision.

With the demonstrated expertise to create what their customers want, and to do so in a profitable manner, the next challenge is to decide where best to allocate those profits.

Reinvestment in the business fuels growth, but the ultimate goal is to harvest it out for personal use.

Along with business growth comes associated tax liabilities that can whittle down both the dividend distribution of profits, and the capital gain on a sale. And as irritating as it is to pay tax on an actual sale by the owner, a deemed disposition on that owner’s death can be even more costly and disruptive.

Life insurance has long been a cost-effective way for small premiums to fund a large cash need, like tax on death. Taking it a step further, a policy’s own tax features can enhance current and future value, particularly when combined with a leveraged loan.

Interest is not deductible if a loan is used to obtain life insurance, but can be deductible if its cash surrender value (CSV) is pledged as collateral for a loan used to earn property or business income.

CSV insurance, also known as exempt insurance, allows investment of extra deposits into it:

- Earnings on that excess (up to legislated limits) are tax-exempt while within the policy,

- Payout on death is also tax-exempt, and

- When a death benefit pays to a corporation, as much as 100% may flow out of it tax-exempt.

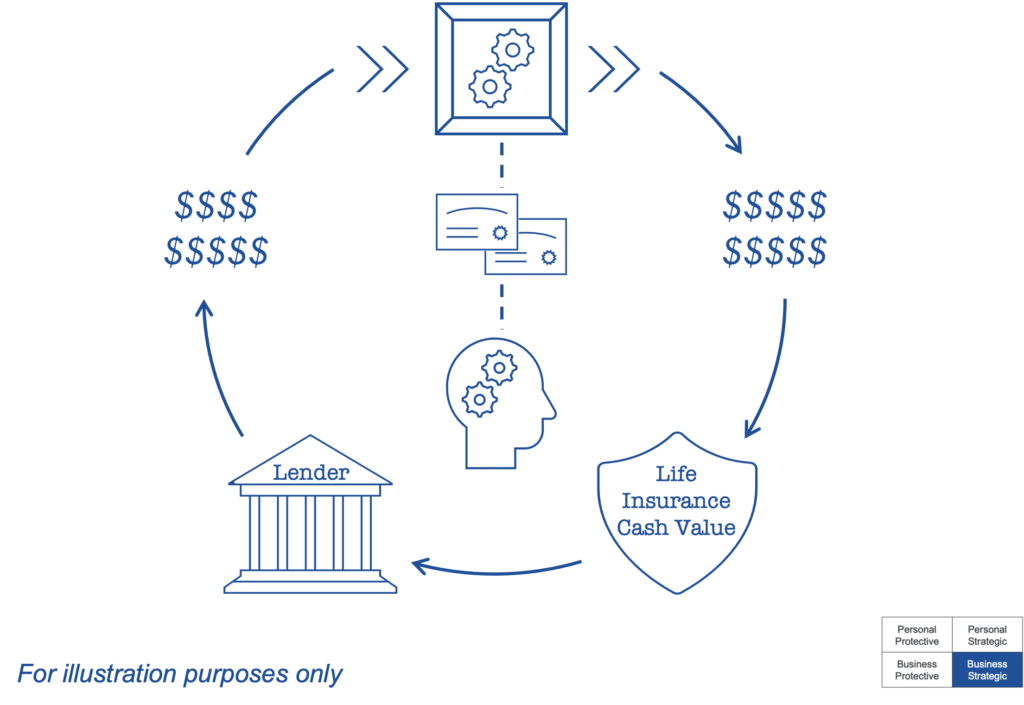

Order of steps is critical to achieve intended results:

- Convert select corporate assets into cash, either as a one-time lump sum action or annual series

- Use cash for annual premiums on exempt life insurance, with excess invested tax-sheltered

- Pledge policy to lender, facilitating loans up to 90% of CSV, or more if other collateral is offered

- Use loan proceeds to re-acquire those corporate assets to continue growing the business

- Interest is deductible, and as the CSV grows, its collateral value enables increased future loans

More complex variations may position the shareholder as the borrower and/or policyholder.