Flexibility in the wake of incapacity

Powers of attorney (POAs) are important tools in estate planning, allowing a grantor[1] to name an attorney to make decisions about oneself and one’s property if incapacity strikes.

This provides a grantor with a high degree of comfort and certainty, knowing that an attorney can act both proactively ahead of complications that may appear on the horizon, and reactively as unexpected events transpire that call for adjustments.

Limits on an attorney’s power

On the property front, an attorney can generally do anything a grantor could do, except make a “testamentary disposition”, being a change of rights that takes effect on death but can be revoked while living. The most familiar example is a gift in a Will, with many courts having extended this logic to registered plan beneficiary designations.

While an attorney is a fiduciary who is required to act in the best interests of the grantor, that power may at times be abused. Accordingly, it makes sense to have limitations, but those can simultaneously be a practical impediment if appropriate changes cannot be made by an attorney, despite being to the benefit of a grantor.

Change in circumstances

Here are some situations where an inability to revisit a beneficiary designation could be problematic:

- Retirement income – RRSPs are usually transferred to RRIFs once income is needed — which may in fact be accelerated on incapacity — and that’s mandatory for RRSPs at 71. If remaining in RRSP form, withholding tax is higher on withdrawals, and there’s no ability to reduce tax with the pension credit or pension income splitting.

- Change of financial institution – The attorney may wish to consolidate assets to simplify oversight, as well as to revisit portfolio risk given the likely change in the incapacitated person’s lifestyle needs and life expectancy.

- Pre-deceasing beneficiary – The interest of a pre-deceasing beneficiary is distributed proportionately among all other beneficiaries. While contingencies are possible, financial institutions will not allow complex rules. There could also be probate tax and creditor exposure in the eventual estate if no beneficiary remains on the plan.

- Change of province – If a person moves to another province, preferably their assets will move with them. This will be especially helpful if moving to a province that provides lifetime creditor protection on RRSPs and RRIFs.

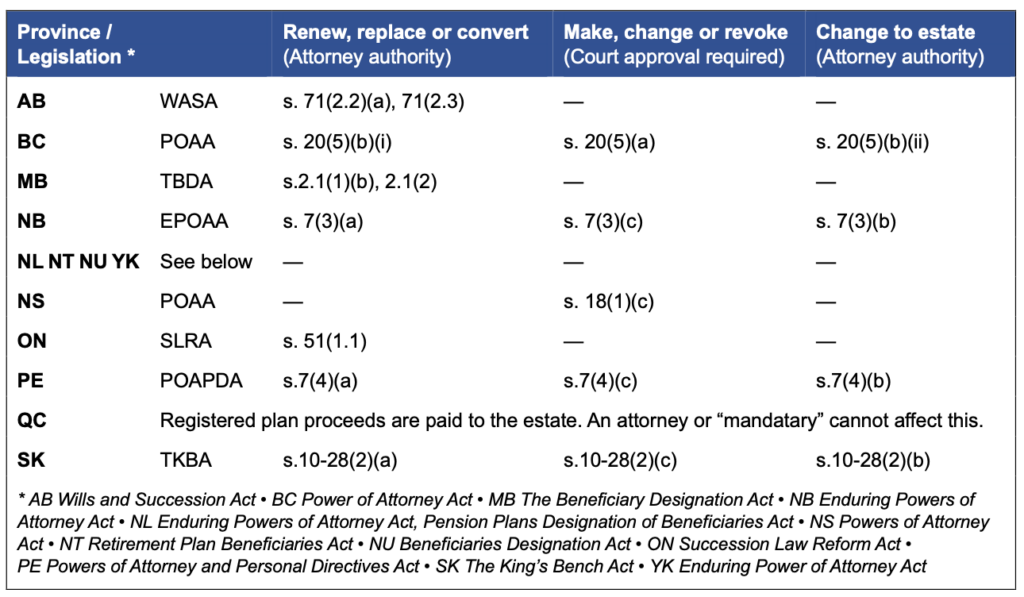

Summary by province

The following table outlines what an attorney can and can’t do, according to the province where the grantor executed the POA document. The relevant legislation must be consulted to be certain of the scope of activity allowed, with three general categories available:

- Renew, replace or convert – If applicable, the attorney may designate the same person(s) on the same type of new/receiving plan as had been executed by the grantor on the originating plan.

- Make, change or revoke – With approval of a court, the attorney may make a change to a designation that does not have to be a carryover of a past/original designation.

- Change to estate – An attorney, without having to seek court approval, can change the designation from whatever it is presently to the estate of the grantor.

To give effect to some provisions, it is sufficient if an attorney is validly appointed, while others require that the POA document explicitly authorizes beneficiary changes. Again, it is critical to consult the relevant legislation, and ideally for the attorney to obtain legal advice before taking any action.

[1] “Attorney” and “grantor” are used for consistency in this article, though terms vary some by province.