How tax integration protects against double-taxation

As a business owner, you have a few options when choosing the legal structure for providing your goods and services – most commonly a sole proprietorship, partnership or corporation.

There can tax benefits using a corporation, but there is also more complexity to understand and manage.

Business structures

With a sole proprietorship, you are taxed on the net income from the business after deducting expenses. The net income is taxed to you personally, at progressively higher rates as your income rises, as is the case when you earn other types of income personally. A business loss can be deducted against current income, or be carried to offset business income in past or future years. (The details of loss usage are beyond the scope of this article.)

A partnership does not pay tax. Rather, the partners report their respective share of the partnership’s income or loss as their own.

Unlike a sole proprietorship or partnership, a corporation is clearly distinguished as a separate legal entity from those who own and operate it. It is taxable on the business income, and the distribution of that income to its shareholder/owners is subject to further tax, with rules in place to protect against double-taxation, as discussed below. Losses can be used by a corporation (again with carryback and carryforward rules), but cannot be transferred to shareholders.

Limited liability of corporations

Leaving aside tax for the moment, the fact that a corporation is a separate legal entity from its owner/shareholders means that it can potentially limit the liability of its owners. If a corporation accumulates large debts or is sued, shareholders’ personal exposure is generally capped at – or “limited” – to losing their investment in the corporation. If the corporation’s assets are exhausted, creditor/claimants cannot pursue shareholders personally to satisfy those corporate debts.

Even so, it is not uncommon that shareholders of a new or small corporation will be required to give personal guarantees to obtain financing or trade credit, so limited liability has its own practical limitations.

Incorporated professionals

Incorporation is available to many professionals, including accountants, medical professionals, engineers and lawyers. The provincial governing body for the profession should be consulted to determine its availability and any restrictions.

Professional corporations also limit liability for general business dealings, but there is no such shield against malpractice claims. The professional remains personally responsible for the services and advice given, for which the professional will be required to carry appropriate liability insurance as a condition of the license to practice.

Tax aspects of incorporation

As noted, a corporation is taxed on its business income, then tax is also levied when it distributes its income to its shareholders. To the extent that the net income is not needed for current personal needs, the excess could be left in the corporation, deferring the tax eventually applying to a dividend. If the individual’s marginal tax rate is higher than the applicable corporate rate, more is available to be reinvested in the business.

To give that some context, top personal tax rates are near or beyond the 50% mark, but general corporate rates are in the area of 23% to 31%, and small business corporate rates (on active business income up to $500,000 in most provinces) range roughly from 9% to 12%. The variance depends on the provincial rates where a corporation is resident, with federal rates being consistent across the country.

Our tax system integrates the corporate and personal tax rates to protect against double-taxation. Specifically, it is set up so that about the same amount of tax is paid whether income is earned personally, or through a corporation then paid as a dividend to a shareholder.

There are two main devices used to achieve this integration.

Dividend gross-up

- When a dividend is paid, it is grossed-up by an arithmetic factor that approximates the original income the corporation earned.

- This grossed-up amount is added to the shareholder’s other income, essentially emulating the shareholder as being the original earner of the actual corporate income.

- An initial tax figure is derived by applying the tax rates at that individual’s progressive tax brackets.

Dividend tax credit

- The shareholder is then given a credit (a reduction in personal tax) based on the estimated tax the corporation paid on the income that fed into the dividend amount.

- In effect, the shareholder pays the difference or top-up to the tax already collected from the corporation.

- At very low personal tax brackets it is possible that the tax credit is less than the initially calculated tax due.

In such situations, the effective tax rate is negative, allowing the excess credit to reduce tax on other income.

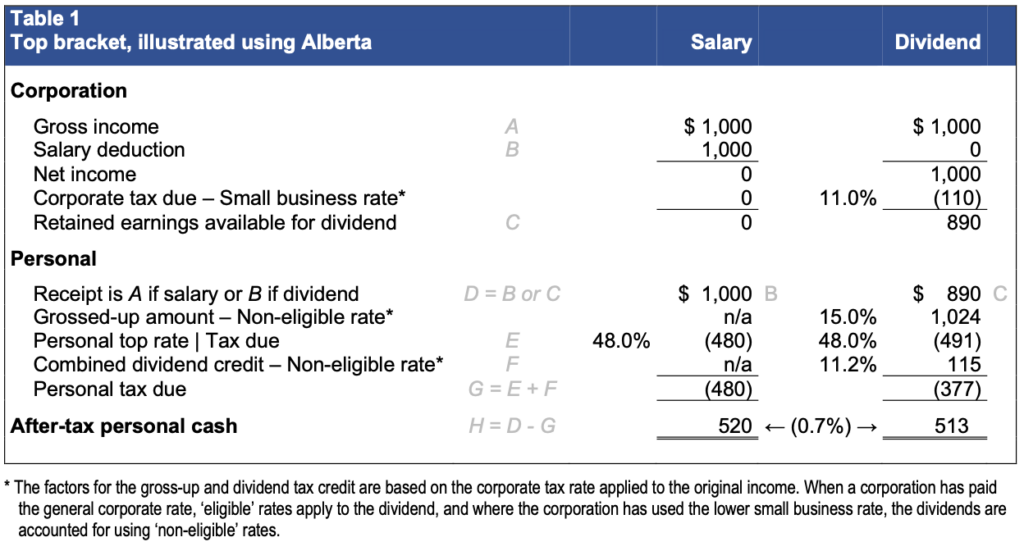

Illustrating integration between corporation and shareholder

Detailed integration comparison

In principle, the process works at all income levels, but it can be most clearly illustrated at top tax bracket. To show this, we’ll use the 2026 Alberta rates.

Net integration summary, all provinces

The gross-up is the same for all provinces, as is the federal tax credit. The provincial tax credit varies by province. Table 2 shows the net after-tax personal cash for all provinces at top bracket, showing for example the final row H from Table 1 as the Alberta column in Table 2.

As Table 2 shows, the net tax difference when earning through a corporation then paying a shareholder dividend is negative 1.7% to positive 0.7% as compared to paying a salary to that same person as an employee. While this is not the whole story, the small difference in result emphasizes that tax alone should not be the determinant whether to incorporate.

Cost considerations before incorporation

As discussed, if not all the income is needed for immediate personal spending, there is a deferral benefit to earning through a corporation. On the other hand, there are higher accounting and legal start-up fees, and ongoing costs to using a corporation. Professional advice should be obtained to get a full picture before deciding how to proceed.