Strategies to defer and reduce tax on capital gains

Mutual funds provide a streamlined way to make a single purchase into a portfolio of securities. By pooling with others, an investor has a cost-effective way to participate in a chosen investment mandate that would be difficult to assemble individually.

Over time though, changes in the investment landscape, securities regulations and tax rules may prompt an investment manager to merge funds. This happens for a variety of reasons, usually designed to reduce overlapping mandates, simplify product offerings and achieve better economies of scale.

From an investment perspective, all investors should inform themselves of the mandate and strategies of the continuing fund.

From a tax point of view, it is those in non-registered accounts who may be most affected, with the prospect of capital gains being triggered either by the investor selling prior to the merger, or upon the investment manager completing the fund merger.

1. Capital gains generally

Mutual funds offer investors the potential for both income and capital gains. Income is what is earned from the invested capital, generally distributed annually in the form of interest and dividends. A capital gain is an appreciation in the value of the invested capital itself.

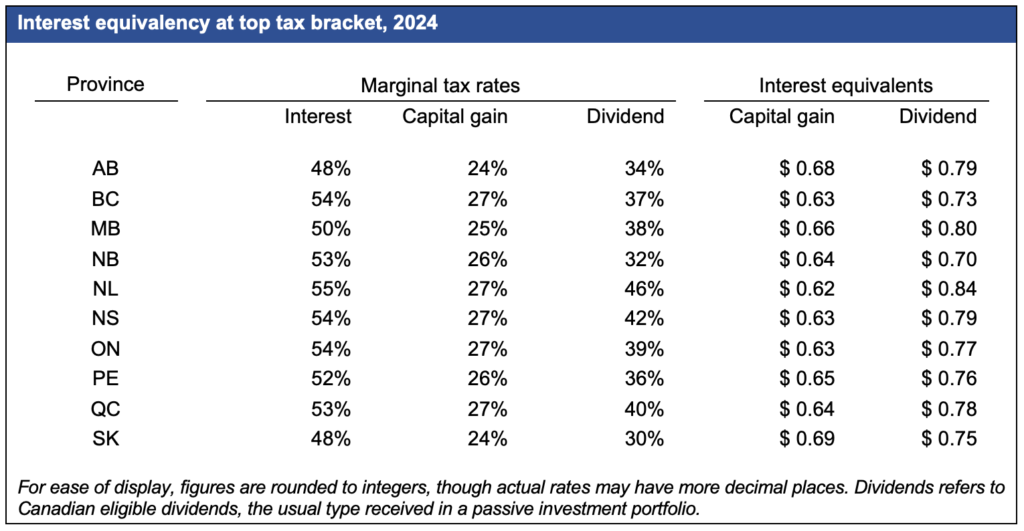

An increase in price is an unrealized capital gain, with no tax applying to such a price movement. However, once there is a sale or disposition, capital gains become realized and taxable. Since 2000, 1/2 of a capital gain has been included in income. In the 2024 Federal Budget, the inclusion rate was increased to 2/3, but the 1/2 rate remains available for individuals on the first $250,000 of capital gains in any year. For trusts and corporations, the 2/3 rate applies to all capital gains.

A mutual fund investor can experience capital gains in a few ways:

-

- If the investor sells some or all of a mutual fund that has appreciated in value (owing to the appreciation of its underlying holdings), the investor will realize a capital gain directly.

- Within the mutual fund, the buying and selling of securities can result in net capital gains for the fund, which are then distributed proportionately to investors.

- In the case of a fund merger, a capital gain may arise from the combined effect of dispositions within the merging fund and the investor disposition of that fund in the course of moving to the continuing fund.

The investment manager’s management information circular will give general guidance on expected tax effects of a fund merger. The investor may then consider the following strategies to reduce or eliminate any resulting tax liability.

2. Applying capital losses

Just as an appreciation in the price of a security is a capital gain, a decrease in price is a capital loss. As with capital gains, capital losses are unrealized until there is a taxable event.

Capital losses realized in a year must be used against capital gains that same year, with the investor then having discretion to apply any unused excess against capital gains in any of the three preceding tax years, or to carry forward for future use.

a. Use your capital loss carryover

If you have unused capital losses from past years, you may apply them against capital gains in the current year. You can find your carryover balance on your latest Notice of Assessment, or by logging into your My Account on the Canada Revenue Agency website, and viewing “Carryover amounts” under the “Tax returns” tab.

b. Review current holdings for loss positions

Look at your current non-registered account holdings to see if you have any securities in a loss position. You can sell a portion of those to realize sufficient capital losses to offset some or all of the capital gains arising out of a fund merger. To be clear, the tax impact contributes into your decision, but should not dictate your actions.

In fact, a common concern in this situation is the possibility of missing out on a price recovery of those disposed securities. While it may be tempting to immediately re-establish the position after triggering a loss, tax must again be borne in mind, due to the risk of being caught by the superficial loss rules in the Income Tax Act (ITA).

Superficial loss rules

These rules apply if the same security is purchased in the 30 days before or 30 days after the loss transaction. This extends beyond you as the purchaser to affiliated persons, including your spouse and registered plans belonging to either of you, such as RRSPs and TFSAs. The capital loss is denied on the sale transaction, but an equivalent amount is added to the adjusted cost base (ACB) of the new holding on the purchase side. Thus, the capital loss remains available for the holder to use in future, but cannot be used against capital gains arising out of the fund merger presently. An important exception is that if the purchase transaction occurs in a tax-sheltered account where ACB is not applicable (eg., RRSP, TFSA, etc.), the capital loss is forever forfeited.

c. Import losses of a spouse

There is a way to use the superficial loss rules to your benefit if you do not have any securities in a loss position, but your spouse does.

-

- Your spouse sells and realizes a capital loss, and you purchase the same security in the +30/-30 day window.

- Your ACB will be higher than your purchase price by the amount of the added loss denied to your spouse.

- After waiting at least 30 days following your spouse’s settlement date (which is 1 day after the transaction date), you can sell and realize your loss so you can use it against the capital gain from the fund merger.

Of course, the price of your new security could rise during your holding period, reducing your expected loss. But that means you receive more money when you sell, so there’s not much to complain about under that scenario.

d. Accessing losses of an owned corporation

An investor who is the owner/shareholder of a corporation could transfer the appreciated mutual fund holding to that corporation. Unlike an arm’s length transaction, this transfer can happen on a tax-deferred basis by electing a rollover under ITA section 85. If the transfer occurs prior to the fund merger, the corporation will be the investor that is taxed on any deemed capital gains, against which it may apply any existing capital losses. Depending on the corporation’s year-end, any excess gain may be realized in either the current or next calendar year.

Consult qualified business and tax professionals to review how this may affect and be influenced by relative personal and corporate tax rates, the corporation’s small business threshold and the tax on split income (TOSI).

e. Trust distributions, rollouts and other interactions

If the investor is a trust, a closer look at its tax attributes and those of its beneficiaries may reveal planning options. Most trusts are taxed at the top marginal tax bracket, but some are entitled to graduated bracket treatment. Trust income is generally distributable to income beneficiaries, and capital property may be rolled over to capital beneficiaries at ACB. While capital losses may not be distributed from a trust to beneficiaries, if one or more beneficiaries have existing capital losses or securities in a loss position, this could inform their combined planning.

3. Sell to family to spread the tax up to 5 years

If you sell capital property but do not receive all the proceeds immediately, you can claim a capital gains reserve that allows you to recognize the gain over as many as 5 taxation years. In fact, there is a way that you may be able to do this with a spouse or other family member.

Your family member purchases your current holding prior to the merger, giving you 1/5 of the price plus a promissory note at the prescribed interest rate applicable to spousal/non-arm’s length loans. The prescribed rate is adjusted quarterly according to economic conditions, standing at 5% for the third and fourth quarters of 2024. As owner of record at time of the merger, the family member would be taxed on the capital gain arising at that time. As the loan is retired over the next four years, you recognize a proportionate gain each year.

This must be a sale directly to the other person, not a redemption of the fund by you and a purchase of the fund from the investment manager by the other person. As well, this assumes that the purchaser has his/her own resources to fulfill the transaction; if not, this is not a viable option.

Consult qualified tax and investment professionals to make sure that all necessary steps are taken, that they are in the right order and that everything is adequately documented.

4. Defer other income sources

If you have some control and flexibility with your income sources, you could defer or otherwise adjust them:

-

- Owner/shareholders of business corporations may reduce salary or dividends, or adjust the mix of them.

- RRIF withdrawals could be limited to mandatory minimums.

- Those on the verge of commencing their CPP retirement pension or OAS pension may consider deferring to the next or later year.

- Sale of a cottage or investment property with its own unrealized capital gain might be deferred to the next or later year. Alternatively, the transaction could be structured so that payments are spread over multiple years, whether with family or a willing arm’s length purchaser, to take advantage of the capital gains reserve rules.

- At tax filing time, recipients of eligible pension income can choose to split the appropriate amount with a spouse (subject to the 50% maximum) that will minimize the tax bill for the couple.

Bear in mind that while a fund merger may trigger a capital gain, there will not generally be a cash distribution. This may limit how much these deferrals may be used if there is insufficient cash for living expenses. As a complement to the deferral of these taxable sources above, one might consider a larger than usual TFSA drawdown for the current year.

5. Charitable donations in-kind

The tax system provides generous assistance for those who donate to charity. Beyond the first $200 of annual donations, the tax credit rate is around 50%, varying by province. In effect, about half of the value of the donated property comes back to the donor/taxpayer in the form of reduced tax on other income.

Cash is common for small donations, but the tax benefits are accentuated when other forms of donation are used. In particular, when appreciated securities are donated in-kind, there is no tax to the donor on as-yet unrealized capital gains. A donation prior to the fund merger can take advantage of this rule, but first confirm that the charity’s bylaws allow it to accept securities and that it has a brokerage account ready to receive them.

6. Create deductions

If an investor has available room and cash for the purpose, contributions into an RRSP will allow for a deduction against income in the current year.

For investors who have the investment knowledge, qualified risk tolerance and financial capacity, an investment loan could be arranged. Interest can be deductible if the loan proceeds are directed toward producing income in a non-registered account. Interest can also be deductible on loans taken out for business purposes. In either case, consultation with qualified business, tax and investment professionals is highly recommended.

7. Consult your tax professional

This article provides information about potential tax issues arising out of mutual fund mergers, and strategies an investor may take in response. This is neither advice nor a recommendation for an investor to take any action and no member of the Aviso Wealth group is capable of providing tax advice in any circumstances. Readers are advised to consult a qualified tax professional to provide advice based on individual circumstances.