[Eight-part series, current to publication date only]

1 – Why and how do we prepare

2 – Finding the right buyer

3 – Getting the best price

4 – Tax issues overview

5 – Incorporation issues overview

6 – Caveats and limitations

7 – Selling when incorporated vs. unincorporated?

8 – Ways to get paid

8 – Ways to get paid

We’ve reached the end of our eight-part series on how to sell your book. This article discusses options for getting paid.

Lump sum

If a buyer has the funds available and the parties reach an agreement, the transaction may be carried out with a lump sum payment on closing.

If the buyer is not an employee and has obtained purchase financing to carry out the transaction, the annual cost of interest should be a deductible expense. On the receiving end, any payments attributable to interest are fully taxable to the seller. This occurs even though the transaction is capital in nature, and regardless of whether it’s an asset or share sale.

Instalments and earnouts

If the parties decide to spread payments across several years, it should not affect the tax treatment for either party—so long as future payment is not based on production. This may occur so the buyer doesn’t have to come up with a large sum all at once.

If it’s an asset sale, the seller may be able to take a capital gains reserve, allowing for a portion of those gains to be recognized and taxed in future years.

If the sale is of goodwill/a client list, the terminal allowance on the eligible capital property must still be recognized at closing; this would mean the seller would pay all taxes in the year of closing, despite some proceeds being not yet received. [New regime: The 2016 Federal Budget will replace the eligible capital property (ECP) tax regime with a capital cost allowance class (for details, see advisor.ca/ECP). There is a transitional period, so we’ll still discuss the legacy ECP regime, but be aware that new rules are coming in 2017.]

Where future payments are calculated with reference to the actual income earned from the book or practice, the tax treatment can vary, especially for the seller. This kind of arrangement is known as an “earnout,” with the intention being to assure (for the buyer, especially) the value of the practice/book is properly reflected in the final agreement.

The drawback of this arrangement to the seller is that those directly tracked payments will be taxed as income, though recognition would be deferred for payments received in future years.

The relevant section of the ITA is s. 12(1)(g) (see below), with CRA’s principal interpretation of this provision being in Interpretation Bulletin IT-462 (see below).

Income inclusion under ITA s.12(1)(g)

“Payments based on production or use—any amount received by the taxpayer in the year that was dependent on the use of or production from property whether or not that amount was an instalment of the sale price of the property, except that an instalment of the sale price of agricultural land is not included by virtue of this paragraph.”

CRA IT-462: Payments based on production or use

For the vendor/seller, income treatment will apply if the payments are entirely based on production/use, per s. 12(1)(g). If the payment is structured as fixed sum plus some amount based on production/use, the former is proceeds of disposition (i.e., capital treatment), and the latter is income. Where there is a minimum payment dependent on production/use, that is income; however, any top-up to the minimum will be proceeds of disposition. A payment structured as a maximum at closing with potential future reduction/adjustment would be treated as proceeds of disposition, but income treatment would apply if the arrangement is not reasonable.

For the purchaser/buyer, payments normally constitute cost of capital property, even if the vendor/seller has included some or all as income.

There is an element of unfairness where the parties genuinely cannot determine the final value at the time of closing. The reasonable use of an earnout for business purposes can result in an unsatisfactory result for the buyer in requiring an income inclusion of earnout amounts received pursuant to ITA s.12(1)(g). CRA recognizes this problem, and provides some administrative relief in Interpretation Bulletin IT-426R (see below). The relief only applies to share sales, not asset sales.

IT-426R ARCHIVED—Shares Sold Subject to an Earnout Agreement

A vendor/seller may use the “cost recovery method” to record the receipt of future payments effectively as capital gains. This applies to share transactions where the parties are at arm’s length, the earnout relates to underlying goodwill that cannot reasonably be determined at closing, and the vendor/seller is resident in Canada.

The earnout may be no longer than five years.

A copy of the sale agreement must be attached to vendor/seller’s tax return for the year of closing, together with a letter requesting application of the cost recovery method.

A transaction structured with a maximum amount paid up-front and potential deduction if certain conditions are not met (mentioned in IT-462) is known as a “reverse earnout.” Note that it requires that the buyer pay the full purchase price at closing, and also that the seller generally record the full disposition in the year of closing.

As the reverse earnout likely reflects the fact that the parties have not determined the final proceeds of disposition, a capital gains reserve may not be taken, meaning that the capital gain must be realized in the year of closing.

2013-0505391E5 F—Clause de earnout renversé

Is it possible to deduct an amount on account of the capital gains reserve where there is a reverse earnout agreement in a share purchase agreement? CRA has said no. Proceeds of disposition are not certain at the moment of disposition, which is one of the requirements to be eligible to deduct an amount as a capital gains reserve.

Earnouts and reverse earnouts are not available for asset sales. Using either arrangement will result in income treatment for the seller, where eligible capital property might have otherwise applied.

2004-0098121E5 (E)—Goodwill Sold Subject to an Earnout Agreement

This CRA letter addressed whether an earnout in an asset sale would qualify under the definition of cumulative eligible capital, or alternatively if the cost recovery method under IT-426R could be used. The CRA representative stated that where the consideration received for eligible capital property is dependent upon the use or production from that property and no amount can be quantified at the time of sale, such consideration is not an eligible capital amount but is taxable as income under paragraph 12(1)(g). Furthermore, the cost recovery method is only available on a share sale.

Smith v R. deals with a case where a combination of fixed and variable payments was attempted. On their own, the agreed upon fixed amounts would likely have enabled the seller to claim them as proceeds of disposition. However, the payments were subject to a price adjustment clause calculation based on actual commissions earned, with unfortunate tax results for the seller.

Smith v R., 2011 TCC 461

A property/casualty brokerage was purchasing a client list. The price was based on $156,000 in current commissions, times a 2.25 acquisition factor, totaling $351,000. Payments were set at 40% in the closing year and 20% each of the next three years, with annual interest payments for remaining outstanding amounts. A price adjustment clause adjusted the annual payments based on actual commissions earned from the clientele. The court found that the price was not fixed and determined, but was instead dependent on actual commissions. All amounts (not just the post-closing amounts) were determined to be taxable per s.12(1)(g). Interest was taxable as investment income per s.12(1)(c).

Interest on payments

As mentioned earlier, interest payments are treated as income to the seller/recipient, and are generally a deduction to the buyer/payer.

Income inclusion—ITA s.12(1 c)

“Interest—subject to subsections (3) and (4.1), any amount received or receivable by the taxpayer in the year (depending on the method regularly followed by the taxpayer in computing the taxpayer’s income) as, on account of, in lieu of payment of or in satisfaction of, interest to the extent that the interest was not included in computing the taxpayer’s income for a preceding taxation year”

Interest deduction related to acquiring business or property—ITA s.20(1)(c)(ii) (partial extract)

“an amount paid in the year or payable in respect of the year … pursuant to a legal obligation to pay interest on: … (ii) an amount payable for property acquired for the purpose of gaining or producing income from the property or for the purpose of gaining or producing income from a business.”

Restrictive covenant

It is normal for a buyer to require the seller to grant a restrictive covenant not to compete in future. There is a value to the covenant, in that the seller is foregoing the right to earn income. If no value is explicitly mentioned in the agreement, the value may be implied based on the seller’s circumstances and the scope of the covenant.

Income—restrictive covenants—ITA s.56.4(2) (partial extract)

“There is to be included in computing a taxpayer’s income for a taxation year the total of all amounts each of which is an amount in respect of a restrictive covenant of the taxpayer that is received or receivable in the taxation year by the taxpayer or by a taxpayer with whom the taxpayer does not deal at arm’s length.”

There’s no income inclusion if one of the exceptions in ITA s.56.4(3)(a-c) applies. The first exception is where income has already been included as employment income (to avoid double taxation).

The second exception is where the amount relates to the sale of ECP (i.e., goodwill on an asset sale), and the third deals with sale of an eligible interest in a corporation or partnership (in our case, a share sale).

For an ECP or share sale, the parties must jointly file a prescribed form (found on the CRA website) by the seller’s tax-filing deadline for the year of closing. The benefit to the seller is that the tax treatment will mirror that of the underlying transaction (i.e., ECP or capital gain), rather than having the full income inclusion.

While this benefits the seller directly, it also provides a negotiating platform that the buyer may use to influence a lower sale price.

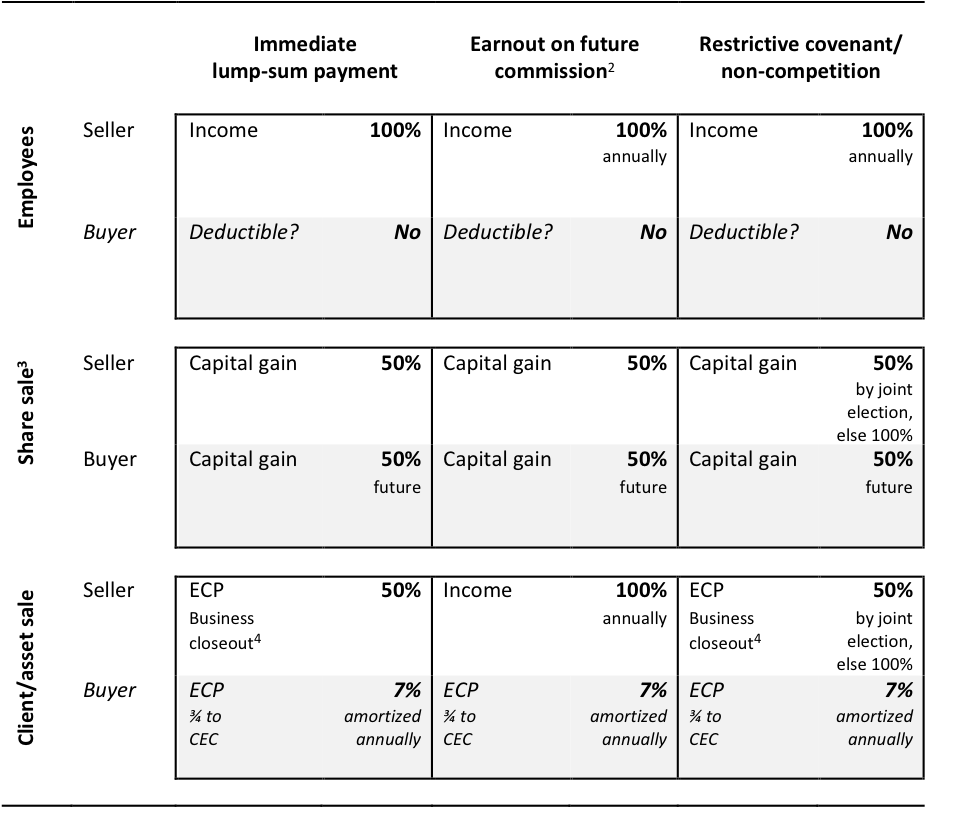

TREATMENT SUMMARY[1]

Notes:

[1] Compiled by Invesco Canada. Uses pre-2017 ECP regime.

[2] Earnout payments on a share sale (not asset sale) that qualify under the cost-recovery method up to five years (per CRA IT 426R2) are entitled to capital treatment. Capital gains reserve normally available up to five years, but not if final price is uncertain (i.e., dependent on earnout or reverse earnout). No reserve allowed for ECP at any time.

[3] Capital gains on share sales are eligible for lifetime capital gains exemption (LCGE) assuming all other requirements are met.

[4] Capital gains-like treatment can arise on the closing of the business and the related disposition of remaining ECP. However, where the seller has claimed past amortization out of the CEC pool, the tax calculation on disposition is more complex.