Early in life, retirement may have seemed like haze on the horizon, but it’s coming into sharper focus now. You’ve enjoyed a successful and satisfying career, though you know that eventually you’ll leave work behind and need to live off your savings.

You’ve been a conscientious contributor to RRSPs and TFSAs, complemented by non-registered savings. But you still have surplus cash available, and as a healthy person with a positive outlook, you’re wondering how you might allow yourself more spending flexibility over an extended lifetime.

In time, you’ll convert your RRSP to a RRIF for your base retirement income, topped-up out of your

non-registered investments. In both cases, tax will shrink your spendable cash, so maybe you’ll dip into your TFSA for a bit more, at least until its exhausted.

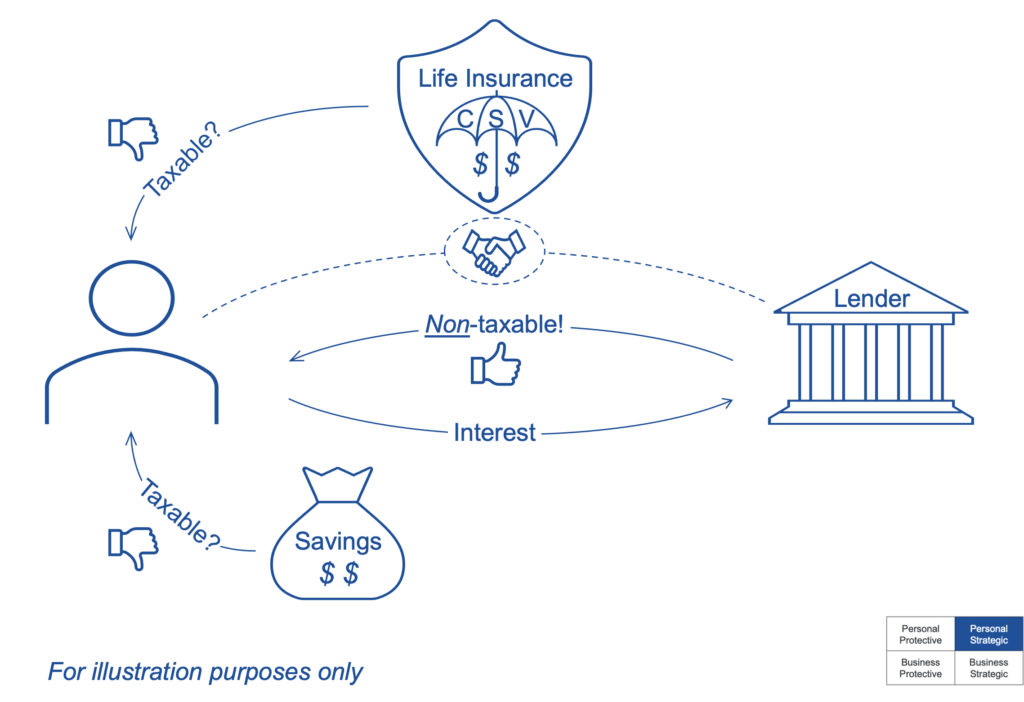

Or, you could take a withdrawal or loan from the cash surrender value (CSV) of a new or existing permanent life insurance policy. Unfortunately, tax may still apply, and the amount taken will reduce the plan proceeds.

Unless there’s a non-taxable way to access that CSV … without affecting the insurance payout – ?

CSV is essentially future premiums in an insurance policy. Tax regulations cap how much money can go into a policy, but meanwhile CSV grows tax-sheltered.

Two types of permanent insurance are appropriate to use here, universal life (UL) or whole life (WL):

- The UL required premium keeps the policy in-force, and the policyholder controls when and how much more to add, and makes all investment decisions

- The WL required premium keeps the policy in-force, and also includes an amount on which the insurer pays dividends to build CSV – with most policies allowing a policyholder to make additional deposits

The key is that the insurance is a supporter but not a substitute for retirement income. Here are the steps:

- Begin with good savings habits and a firm foundation of traditional retirement income sources

- Apply for a UL or WL policy, as suits your investing preference to decide yourself or defer to the insurer

- Make additional deposits into the policy as allowed,

to make optimal use of the tax-sheltering room

- Arrange a loan facility with a lender, pledging the insurance policy and its CSV as collateral

- When desired, draw a lump sum or series of loans, paying interest as agreed – WITHOUT triggering tax

- At death, let the insurance proceeds pay off the loan principal and any remaining interest