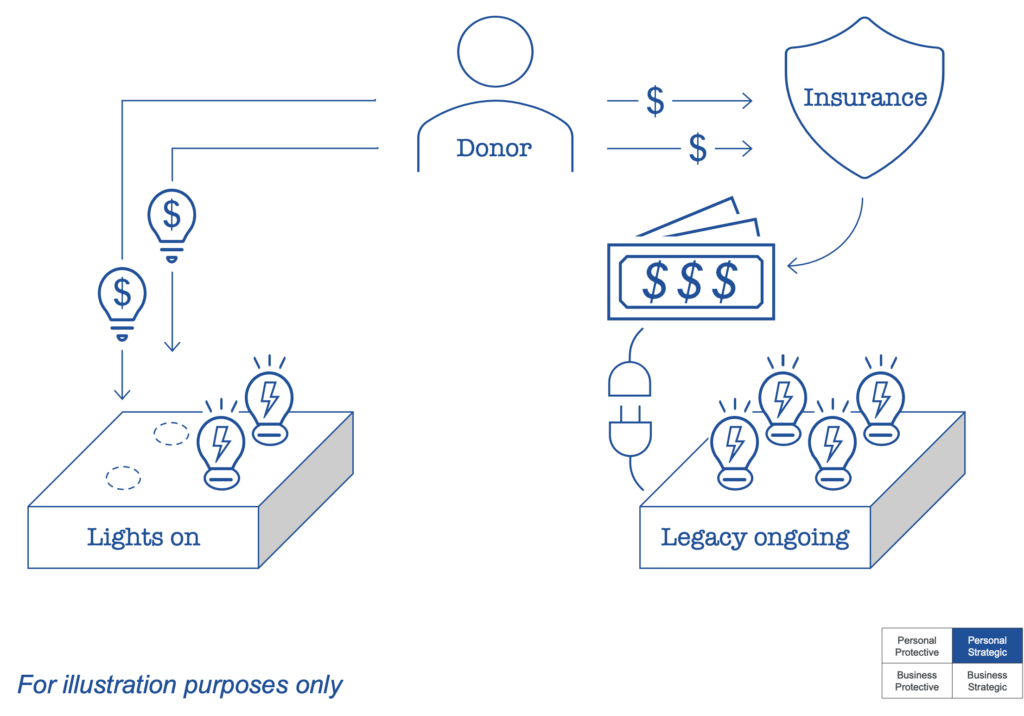

You’re a giver. You support your favourite charities by sharing their message, volunteering your time, and making regular annual donations.

Indeed, most charities depend on consistent financial contributions from loyal backers like you just to keep the lights on. But that leaves precious little to grow the organization, fund capital projects or pursue longer-term strategic initiatives.

So, what can you do to make your contributions even more impactful, especially for future sustainability?

Like those important causes, you too have limited resources. Accordingly, it’s not a matter of simply donating more, but it certainly is possible for you to donate … more strategically.

Strategic for you might mean a lower donation cost where the charity gets the same, whereas strategic for the charity’s benefit might have it getting more, with no change in the out-of-pocket cost to you.

A mutually strategic approach can serve both ends, by naming a charity as beneficiary of a life insurance policy, offsetting up to 100% of final year taxes.

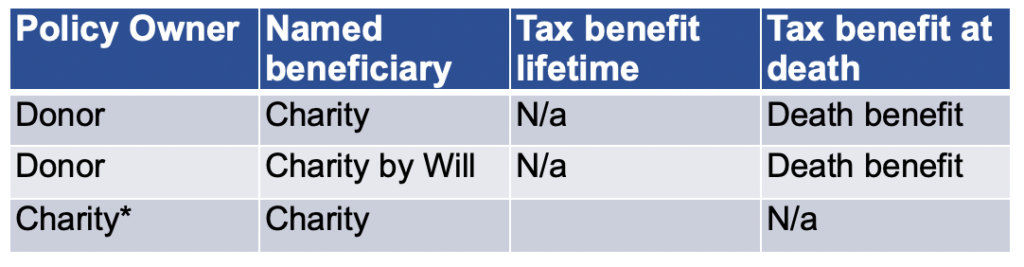

Here are common options for owning the insurance:

* For the 3rd option, a new policy may be issued to the Charity, or an existing one donated. In the latter case, some tax may arise on that transfer, but the donation receipt for the policy’s cash surrender value (CSV) will equal or exceed that tax.

As noted at the outset, your favoured charities have ongoing cash needs, aided by you or others, so this

is not a suggestion to fully divert current donations into insurance. Rather, the issue is whether and to what extent you may wish to shift your emphasis from current needs to future needs, and how to go about it.

Returning to the option of donating an existing policy, note that the CSV is a reserve for payment of future premiums, allowing you to continue your annual cash donations if you wish. And if any future premiums are ultimately needed, either the Charity can pay them, or if you do so then you’ll get a corresponding tax receipt.