We can be living life to the fullest and still get stopped cold in our tracks when a random health crisis strikes. That could be a heart attack, stroke, cancer or a range of other life-threatening conditions.

Whichever form a critical illness takes, the physical symptoms may be the most obvious, but they are bound to be accompanied by mental stress and financial worries. And we’re not talking about the affected person alone, as the emotional and economic impact will be felt throughout the family.

By definition, a ‘critical’ illness calls for an urgent and intensive response, with a real threat of death if treatment is delayed. Whether it’s you needing a leave from employment for your own treatment, or you as spouse or parent supporting an ill family member, it can be a massive disruption.

Unfortunately, regardless of your work situation, the cost of treatment can be a major hurdle to overcome. Bravely, you may believe that ‘money is no obstacle’, but such hopeful defiance will seldom be enough to adequately respond.

Critical illness insurance (CI) is what is known in insurance parlance as a living benefit. Disability insurance (DI) is perhaps more familiar in this category, but whereas DI replaces a portion of income if a person cannot work, CI does not depend on an individual’s earning status.

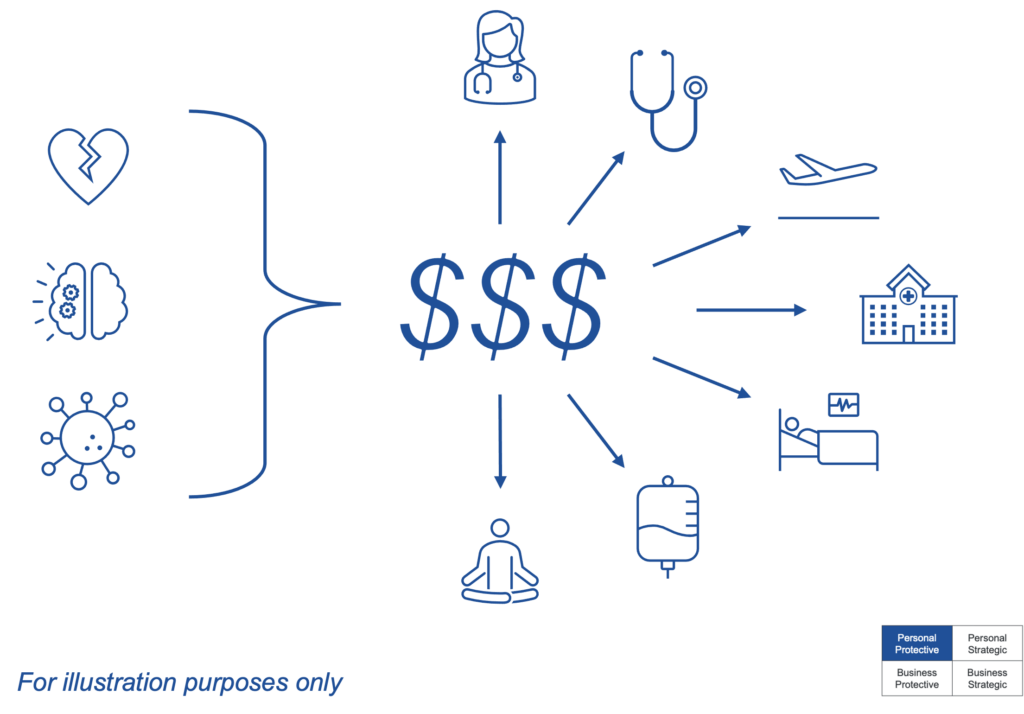

CI is triggered once a person is confirmed to have a qualifying condition, generally paid 30 days after diagnosis. It is a tax-free lump sum payment, including return of premiums if opted at the outset, with NO RESTRICTION on how you spend it.

It is entirely up to you how to use CI proceeds:

- A second opinion from your chosen specialist (with this included by most insurers anyway)

- Diagnostic tests not covered by health insurance

- Specialty treatment/surgery at a medical facility with a reputation for your specific condition

- Out-of-province/out-of-country travel cost for patient, as well as supporting family if desired

- If the local surgery/treatment queue is too long, jump to the head of the line elsewhere

- Prescriptions not covered by health insurance, and/or alternative medications or procedures

- Non-medical respite travel for patient and family, between treatments or in post-treatment recovery